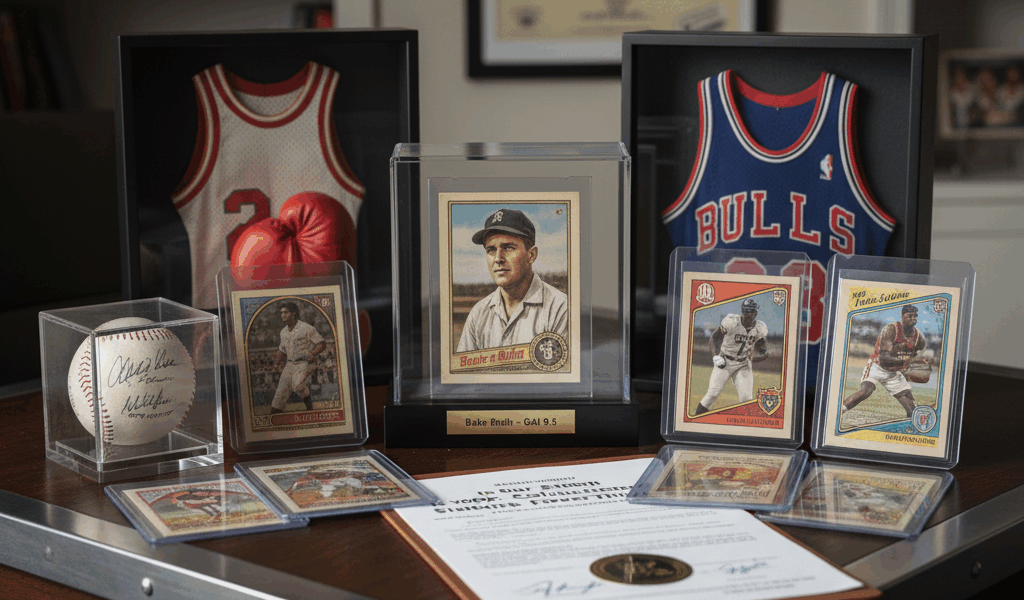

Sports card insurance has gotten complicated with all the coverage options and policy exclusions flying around. As someone who learned about insurance gaps the hard way after a minor flood, I learned everything there is to know about protecting high-value collections. Today, I will share it all with you.

What Standard Homeowners Policies Actually Cover

That’s what makes insurance endearing to us collectors with serious holdings — peace of mind has real value. But standard policies create a false sense of security.

Typical homeowners insurance treats collectibles as “personal property” with strict limits. Most policies cap collectibles coverage between $1,000 and $2,500 total. Your $100K collection? Standard policy might pay $2,000 max after a covered loss.

The Coverage Gap Problem

Probably should have led with this section, honestly. Standard policies fail collectors in multiple ways:

- Low sublimits – Collectibles treated as a category with hard caps

- Actual cash value – Pays depreciated value, not replacement cost

- Mysterious disappearance exclusion – “I can’t find it” isn’t covered

- Theft limitations – May require evidence of forced entry

- Pair and set clause – Won’t pay full value if part of a collection is damaged

Scheduled Coverage

The first upgrade option: schedule individual high-value cards on your policy. This means listing specific items with agreed values. Scheduled items get better coverage and their own limits.

Downsides:

- Each item needs documentation and often appraisal

- You must update the schedule when values change

- Premium increases with every addition

- Not practical for large collections

Collectibles Insurance Policies

Specialized insurers like Collectibles Insurance Services and American Collectors Insurance write policies specifically for sports cards and memorabilia. These typically offer:

- Agreed value coverage (they pay what you insured it for)

- No deductibles or low deductibles

- Broader coverage including mysterious disappearance

- Easier claims processes for collectibles

Documentation Requirements

Whatever coverage you have, document everything:

- Photograph every significant card (front and back)

- Keep grading certificates and receipts

- Maintain a spreadsheet with dates, prices, and conditions

- Store documentation offsite or in cloud backup

Without documentation, claims become nightmares.

Is Insurance Worth It?

Run the math. If you have $50,000 in cards and specialized insurance costs $500 annually, that’s 1% of collection value for protection. Compare that to the total loss scenario.

For serious collections, dedicated insurance usually makes sense. For casual collectors with a few thousand dollars in cards, beefed-up homeowners coverage might suffice.